RBI keeps repo rate unchanged: 5 things fixed deposit investors can do to get better returns

Over the last two weeks, HDFC Bank, HDFC and Bajaj Finance have increased interest rates on their FDs. After the latest status quo announcement by the RBI, more banks may hold interest rate hikes for now. So, after the latest RBI announcement what...

By ET Online | Updated:

Getty Images

After relentlessly cutting interest rates on fixed deposits (FDs) for the past few years, some bank and non-banking finance companies (NBFCs) have started hiking rates. Despite the hike in interest rates by certain banks and NBFCs, the Reserve Bank of India (RBI) has maintained status quo on key rates yet again.

Over the last two weeks, HDFC Bank, HDFC and Bajaj Finance have increased interest rates on their FDs. After the latest status quo announcement by the RBI, more banks may hold interest rate hikes for now.

RBI announced its decision to keep the repo and reverse repo rates unchanged on December 8, 2021 after its bi-monthly monetary policy review. Currently, the repo rate stands at 4% and reverse rate stands at 3.35%. There has been no change in policy rates since May 2020. The repo rate at 4% is lowest since April 2001. Due to lower policy rates, the interest rate on FDs are at multi-years lows.

So, after the latest RBI announcement what should FD investors do to enhance their returns?

Short term deposit rates

It is seen that whenever interest rates begin to rise, short to medium FD rates are hiked first. A week ago, HDFC Bank hiked the interest rates of these FD tenors: 7 to 29 days, 30 to 90 days, 91 days to 6 months, 6 months 1 day to less than one year.

Avoid investing in long-term FDs

It will be better to opt for shorter term deposits when you renew your existing FD or make investments in new FD. By opting for shorter term deposits, say one year or less, in the current scenario, you can avoid locking your money for the long term and take advantage of the interest rate hike as and when it happens.

If you currently lock in your money for the long-term and later break your FD before maturity to re-invest it again at a higher interest rate, then a penalty may be levied.

Use FD ladder strategy to avoid low returns

Currently, interest rates on FDs are at the lowest. How can investors do now to boost their returns? As per financial planners, in the current scenario, this can be done by creating an FD ladder. An FD ladder is created by breaking one big FD into smaller FDs of different tenures.

For instance, if you have an existing FD of Rs 5 lakh, then you can divide it into 5 parts and book 5 FDs of Rs 1 lakh each, of different tenures of 1 year, 2 years, 3 years, 4 years and 5 years. After one year, when the one-year tenure FD matures renew it for 5 years. After two years your FD with 2-year tenure will mature so you can renew it again for next 5 years. Now repeat this exercise each year and your ladder will be ready. This will ensure that not all of your deposits are locked at the lowest interest rate at the same time and your average return is on the higher side.

Look at floating rate options

Investors also have the option to invest in floating rate FDs or floating rate bonds to avoid locking funds for the long term.

Under floating rate FDs, the interest rate on deposits is linked to a benchmark and the interest rate is arrived at with the movement in the benchmark rate. Thus, once the overall interest rate scenario changes and rates start moving up, then depositors will get the real benefit of a floating rate FD as the interest rate on these FDs will also go up.

Currently, Indian Overseas Bank and IDBI Bank offer floating rate term deposits. Apart from banks, an individual has the option to invest in RBI's floating rate bonds too.

RBI floating rate bonds are currently offering interest rate of 7.15% per annum with tenure of 7 years. The interest is payable half-yearly and interest rate is linked to National Savings Certificate (NSC). Any change in the interest rate by the government in the NSC will impact the interest rate of these floating bonds.

Also Read: Government launches 7.15% floating rate bonds: Here's all you need to know

Over the last two weeks, HDFC Bank, HDFC and Bajaj Finance have increased interest rates on their FDs. After the latest status quo announcement by the RBI, more banks may hold interest rate hikes for now.

RBI announced its decision to keep the repo and reverse repo rates unchanged on December 8, 2021 after its bi-monthly monetary policy review. Currently, the repo rate stands at 4% and reverse rate stands at 3.35%. There has been no change in policy rates since May 2020. The repo rate at 4% is lowest since April 2001. Due to lower policy rates, the interest rate on FDs are at multi-years lows.

So, after the latest RBI announcement what should FD investors do to enhance their returns?

Short term deposit rates

It is seen that whenever interest rates begin to rise, short to medium FD rates are hiked first. A week ago, HDFC Bank hiked the interest rates of these FD tenors: 7 to 29 days, 30 to 90 days, 91 days to 6 months, 6 months 1 day to less than one year.

Avoid investing in long-term FDs

It will be better to opt for shorter term deposits when you renew your existing FD or make investments in new FD. By opting for shorter term deposits, say one year or less, in the current scenario, you can avoid locking your money for the long term and take advantage of the interest rate hike as and when it happens.

If you currently lock in your money for the long-term and later break your FD before maturity to re-invest it again at a higher interest rate, then a penalty may be levied.

Use FD ladder strategy to avoid low returns

Currently, interest rates on FDs are at the lowest. How can investors do now to boost their returns? As per financial planners, in the current scenario, this can be done by creating an FD ladder. An FD ladder is created by breaking one big FD into smaller FDs of different tenures.

For instance, if you have an existing FD of Rs 5 lakh, then you can divide it into 5 parts and book 5 FDs of Rs 1 lakh each, of different tenures of 1 year, 2 years, 3 years, 4 years and 5 years. After one year, when the one-year tenure FD matures renew it for 5 years. After two years your FD with 2-year tenure will mature so you can renew it again for next 5 years. Now repeat this exercise each year and your ladder will be ready. This will ensure that not all of your deposits are locked at the lowest interest rate at the same time and your average return is on the higher side.

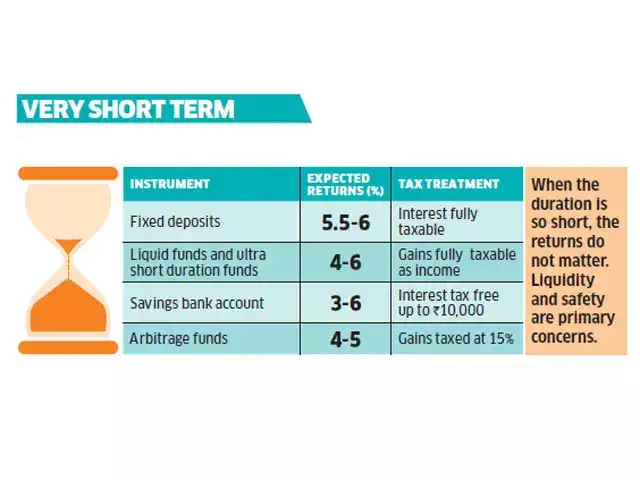

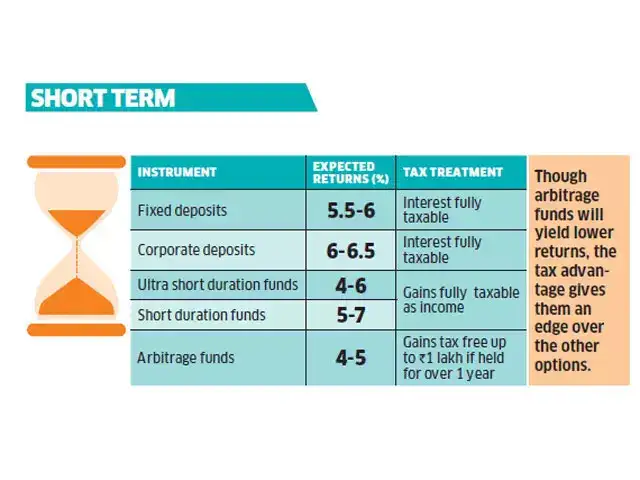

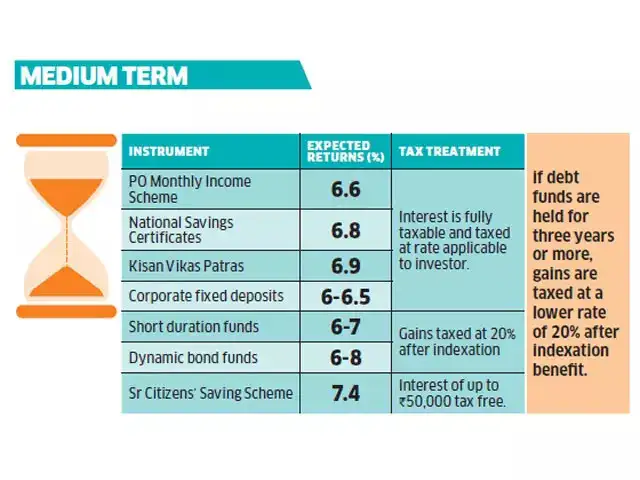

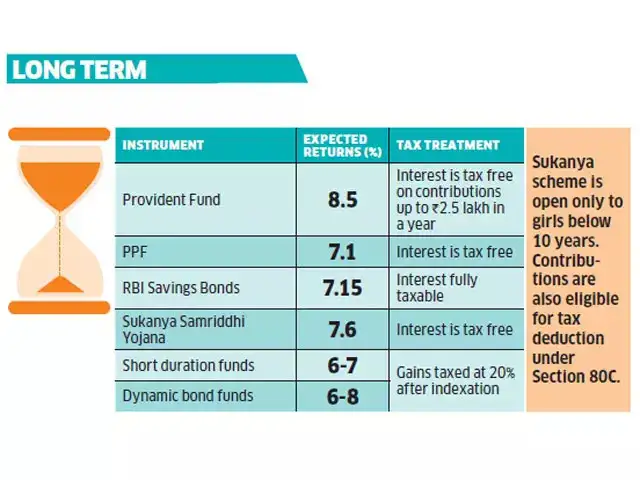

Amid this environment of poor interest rates on fixed deposits and muted returns from other debt options, together with the new taxation rules, investors in the fixed income space should know their utility and goals well. Experts say that it is the time horizon that ultimately determines which fixed income option suits you. Here are suitable instruments on the basis of four broad categories of financial goals, based on distinct investment horizons and income tax treatment of each.

Look at floating rate options

Investors also have the option to invest in floating rate FDs or floating rate bonds to avoid locking funds for the long term.

ADVERTISEMENT

Under floating rate FDs, the interest rate on deposits is linked to a benchmark and the interest rate is arrived at with the movement in the benchmark rate. Thus, once the overall interest rate scenario changes and rates start moving up, then depositors will get the real benefit of a floating rate FD as the interest rate on these FDs will also go up.

Currently, Indian Overseas Bank and IDBI Bank offer floating rate term deposits. Apart from banks, an individual has the option to invest in RBI's floating rate bonds too.

ADVERTISEMENT

RBI floating rate bonds are currently offering interest rate of 7.15% per annum with tenure of 7 years. The interest is payable half-yearly and interest rate is linked to National Savings Certificate (NSC). Any change in the interest rate by the government in the NSC will impact the interest rate of these floating bonds.

Also Read: Government launches 7.15% floating rate bonds: Here's all you need to know

Download

The Economic Times Business News App for the Latest News in Business, Sensex, Stock Market Updates & More.

The Economic Times Business News App for the Latest News in Business, Sensex, Stock Market Updates & More.

Download

The Economic Times News App for Quarterly Results, Latest News in ITR, Business, Share Market, Live Sensex News & More.

The Economic Times News App for Quarterly Results, Latest News in ITR, Business, Share Market, Live Sensex News & More.

Related Articles

RBI looks to revive NRI deposit growth through FCNR(B) route, NRO accounts grow fastest: Bank of Baroda report2026-06-20T07:41:38Z

RBI looks to revive NRI deposit growth through FCNR(B) route, NRO accounts grow fastest: Bank of Baroda report2026-06-20T07:41:38Z- SBI, Axis Bank among lenders set for $2 billion ECB fundraising via RBI swap2026-06-20T00:00:00Z

- RBI revises Kisan Credit Card norms, standardises crop season definition2026-06-19T15:54:25Z

ADVERTISEMENT