SBI PPF account: How to open SBI PPF account online? Get Step by Step process

Once the application gets submitted, a reference number to the Form A will get generated. The reference number allotted will be valid for 30 days from the date of submission and then will be deleted.

By Sneha Kulkarni, ET Online | Updated:

Getty Images

The State Bank of India (SBI) has a wide reach and is present in even the most remote regions. Many people opt to open and invest in Public Provident Fund with SBI.

SBI PPF accounts can be opened at any of the bank's branches across the country.

Here is a look at how one can open a PPF account with SBI online.

Prerequisites to open a PPF account with SBI

Step 1: Log in to the SBI portal at www.onlinesbi.com using your credentials.

Step 2: Under Click on 'Request and enquiries' tab from the top right corner

Step 3: Select 'New PPF Accounts' from the drop-down menu.

Step 4: Displays "New PPF Account" page. The name, address, CIF number, and PAN of the customer will be displayed.

Step 5: If you are opening the account on behalf of a minor, tick the box.

Step 6: Enter your home branch's bank branch code and branch name. In addition, you may provide up to five nominee details based on your preference.

Step 7: Click the 'Submit' button.

Step 8: Once you have double-checked all of the information, click 'Proceed.'

Step 9: Your form has been successfully submitted,' will display in a dialogue box. There will also be a reference number on it.

Step 10: Download the form with the assigned reference number.

Submit the form to the branch with your KYC documents and a photograph within 30 days.

Once the application gets submitted, a reference number to the Form A will get generated. The reference number allotted will be valid for 30 days from the date of submission and then will be deleted. So, within 30 days, you will have to print the account opening form from the tab 'Print PPF Online Application' and visit the branch with KYC documents and a photograph.

Points to note

Also read: Public Provident Fund: 15 lesser known but important rules

SBI PPF accounts can be opened at any of the bank's branches across the country.

Here is a look at how one can open a PPF account with SBI online.

Prerequisites to open a PPF account with SBI

- A savings bank account with SBI

- Aadhaar number must be linked to the savings account.

- Internet or mobile banking must be enabled.

- The PPF account must be linked to an active mobile number.

- An OTP will be issued to the mobile number provided during account registration.

Step 1: Log in to the SBI portal at www.onlinesbi.com using your credentials.

Step 2: Under Click on 'Request and enquiries' tab from the top right corner

Step 3: Select 'New PPF Accounts' from the drop-down menu.

Step 4: Displays "New PPF Account" page. The name, address, CIF number, and PAN of the customer will be displayed.

Step 5: If you are opening the account on behalf of a minor, tick the box.

Step 6: Enter your home branch's bank branch code and branch name. In addition, you may provide up to five nominee details based on your preference.

Step 7: Click the 'Submit' button.

Step 8: Once you have double-checked all of the information, click 'Proceed.'

Step 9: Your form has been successfully submitted,' will display in a dialogue box. There will also be a reference number on it.

Step 10: Download the form with the assigned reference number.

ADVERTISEMENT

Step 11: Print the account opening form from the 'Print PPF Online Application' button.Submit the form to the branch with your KYC documents and a photograph within 30 days.

Once the application gets submitted, a reference number to the Form A will get generated. The reference number allotted will be valid for 30 days from the date of submission and then will be deleted. So, within 30 days, you will have to print the account opening form from the tab 'Print PPF Online Application' and visit the branch with KYC documents and a photograph.

ADVERTISEMENT

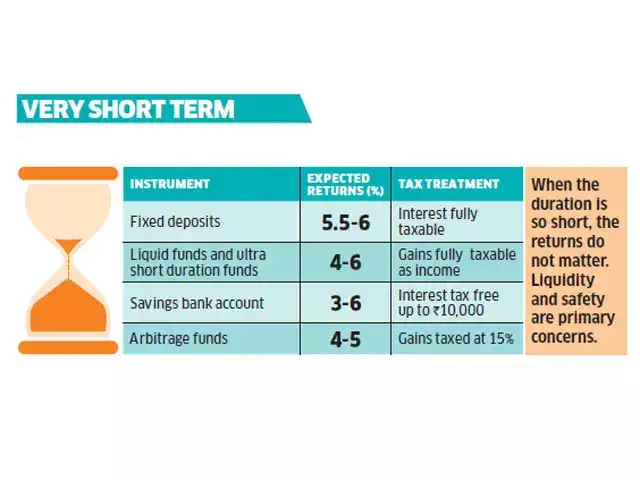

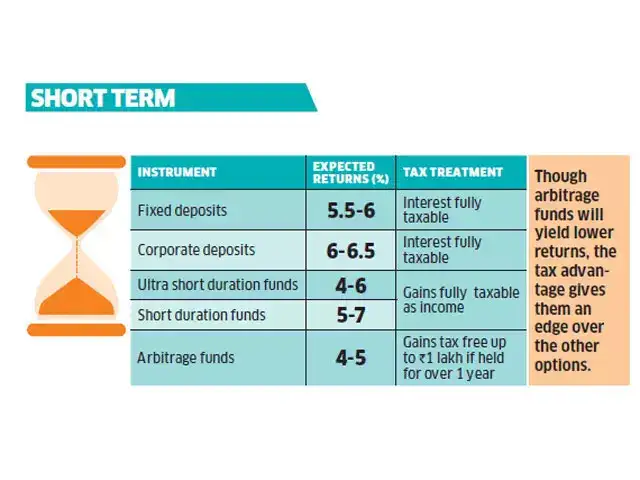

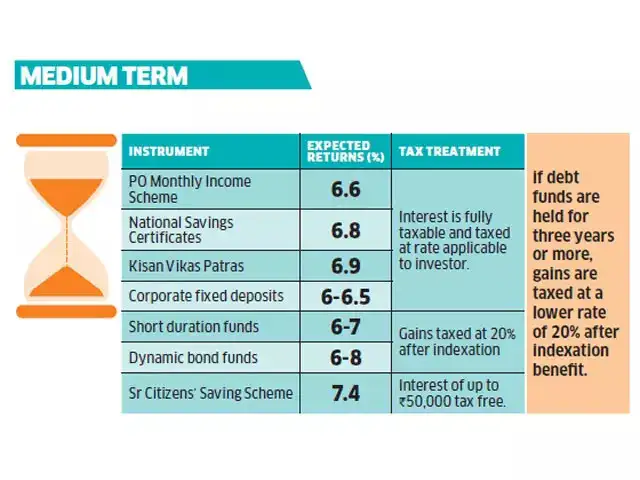

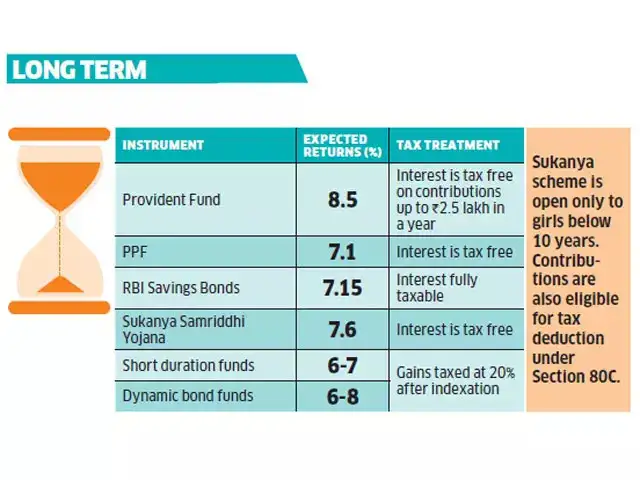

Amid this environment of poor interest rates on fixed deposits and muted returns from other debt options, together with the new taxation rules, investors in the fixed income space should know their utility and goals well. Experts say that it is the time horizon that ultimately determines which fixed income option suits you. Here are suitable instruments on the basis of four broad categories of financial goals, based on distinct investment horizons and income tax treatment of each.

Points to note

- A PPF account has a 15-year lock-in term. However, the account user can choose to extend the term in 5-year tenure

- Individuals can open an account in their own name or on behalf of a minor or a person of unsound mind at any Branch.

- Loans and withdrawals are allowed based on the account's age and balances as of the given dates.

- On the subscriber's request, the account can be transferred to other branches, banks, or Post Offices, and vice versa. The service is provided without charge.

Also read: Public Provident Fund: 15 lesser known but important rules

Download

The Economic Times Business News App for the Latest News in Business, Sensex, Stock Market Updates & More.

The Economic Times Business News App for the Latest News in Business, Sensex, Stock Market Updates & More.

Download

The Economic Times News App for Quarterly Results, Latest News in ITR, Business, Share Market, Live Sensex News & More.

The Economic Times News App for Quarterly Results, Latest News in ITR, Business, Share Market, Live Sensex News & More.

Related Articles

Civil society platform seeks Suvendu help to stop SBI from shifting key centres from Kolkata2026-06-13T14:39:36Z

Civil society platform seeks Suvendu help to stop SBI from shifting key centres from Kolkata2026-06-13T14:39:36Z- Senior citizens FD interest rates up to 8.3%: SBI, HDFC Bank, PNB, ICICI Bank, Axis Bank and more2026-06-13T10:24:31Z

- Eight public sector banks add 13,223 employees in FY26; SBI leads hiring spree2026-06-11T12:10:25Z

ADVERTISEMENT