FD interest rates: Banks offering the highest interest rates on 1-2 years FDs

A fixed deposit (FD) allows you to invest any amount of money for a set period of time at a fixed interest rate. Interest rates on FDs are fixed when the account is opened, and the rate is determined by the length of time you choose to hold the ac...

By Sneha Kulkarni, ET Online | Updated:

Getty Images

A fixed deposit (FD) allows you to invest any amount of money for a set length of time at a specified rate of interest. You receive the payment, plus interest, at the end of the term, which is a good money-saving strategy. Fixed deposit accounts come with a variety of tenures and interest rates.

Interest rates on FDs are set when you start the account, and the rate is determined by the length of time you choose to hold. Depending on your preference, the interest you earn is paid at maturity or on a recurring basis. You are not permitted to withdraw the funds prior to the maturity date. You must pay a penalty if you wish to do so.

The interest rate and type of deposit you select will determine your return on an FD. You can choose from a monthly or quarterly interest payment or reinvestment, which gives you the benefit of compounding.

Here are the banks which are offering highest interest rates in bank fixed deposit for tenure from 1-2 years.

Best 1 year bank FDs

Best 2 years bank FDs

Compiled by ETIG: Data as on March 24, 2022

Loan against FD

While FDs are fixed for a set period of time, you can borrow against them when you need money. You can get up to 70-90% of your FD balance with a loan against it in the form of an overdraft. The advantage is that your FD continues to generate income, and you don't have to withdraw your FD early and risk paying a penalty.

Interest rates on FDs are set when you start the account, and the rate is determined by the length of time you choose to hold. Depending on your preference, the interest you earn is paid at maturity or on a recurring basis. You are not permitted to withdraw the funds prior to the maturity date. You must pay a penalty if you wish to do so.

The interest rate and type of deposit you select will determine your return on an FD. You can choose from a monthly or quarterly interest payment or reinvestment, which gives you the benefit of compounding.

Here are the banks which are offering highest interest rates in bank fixed deposit for tenure from 1-2 years.

Best 1 year bank FDs

| Bank Name | Interest rate (%) Compounded qtrly | What Rs 10,000 will grow into |

| RBL Bank | 6.25 | 10639.80 |

| Indusind Bank | 6.00 | 10613.64 |

| IDFC First Bank | 5.75 | 10587.52 |

| DCB Bank | 5.55 | 10566.66 |

| Karur Vysya Bank | 5.40 | 10551.03 |

Best 2 years bank FDs

| Bank Name | Interest rate (%) Compounded qtrly | What Rs 10,000 will grow into |

| Indusind Bank | 6.50 | 11376.39 |

| RBL Bank | 6.50 | 11376.39 |

| Bandhan Bank | 6.25 | 11320.54 |

| DCB Bank | 6.25 | 11320.54 |

| IDFC First Bank | 5.75 | 11209.55 |

Loan against FD

While FDs are fixed for a set period of time, you can borrow against them when you need money. You can get up to 70-90% of your FD balance with a loan against it in the form of an overdraft. The advantage is that your FD continues to generate income, and you don't have to withdraw your FD early and risk paying a penalty.

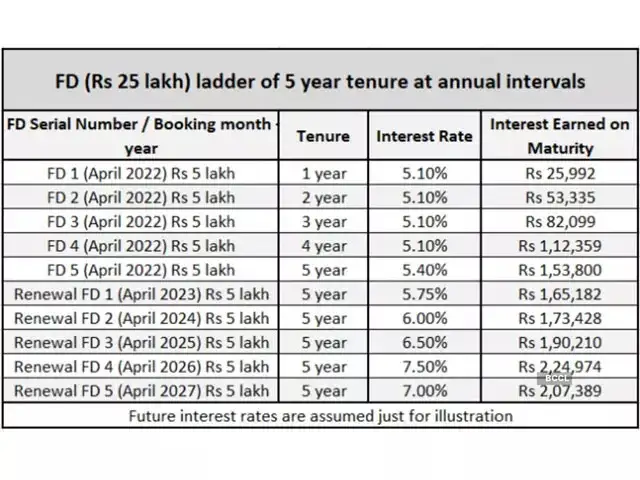

Making an FD ladder is one of the best strategies to manage fixed income instruments. Investors who mainly depend on these instruments, especially senior citizens, can use it effectively to enhance their return and manage liquidity in the investment. When you make an FD ladder, you essentially divide it into parts instead of booking one big FD for the long term.

But why the sudden focus on laddering your fixed deposit investments? That's because the right time to plan an FD ladder is when interest rates start reversing.

Download

The Economic Times Business News App for the Latest News in Business, Sensex, Stock Market Updates & More.

The Economic Times Business News App for the Latest News in Business, Sensex, Stock Market Updates & More.

Download

The Economic Times News App for Quarterly Results, Latest News in ITR, Business, Share Market, Live Sensex News & More.

The Economic Times News App for Quarterly Results, Latest News in ITR, Business, Share Market, Live Sensex News & More.

Related Articles

EPF interest rate retained at 8.25% for FY26

EPF interest rate retained at 8.25% for FY26ADVERTISEMENT