Big jolt for PSU banks: Account portability can break their back

Industry watchers say the move could prove back-breaking for the PSU lenders.

By Rahul Oberoi, ETMarkets.com | Updated:

And you thought easing bad loans will help the PSU bank stocks look up?

A proposal for bank account number portability has come at the worst time for India’s public sector lenders, when they have been desperately looking for ways to get bad loans off their back and raise fresh capital to replenish coffers.

Reserve Bank of India (RBI) Deputy Governor SS Mundra dropped the bombshell on May 30, when he hinted that bank account number portability would be a reality soon.

Industry watchers say the move could prove back-breaking for the PSU lenders and is likely to put private sector lenders with a clear advantage, as they enjoy better operational freedom and are ahead technologically. Such a move can decisively take the banking turf away from the PSU lenders.

Banking analysts, however, say the proposal looks fine only on paper but will be tough to implement on the ground.

Since the arrival of the Narendra Modi-led NDA government on May 26, 2014, private sector banks have been continuously outperforming their public sector peers in the stock market by huge margins. Shares of IndusInd Bank, DCB Bank, Lakshmi Vilas Bank and YES Bank have surged over 150 per cent in the first three years of the Modi government.

Other private sector bank majors such as Kotak Mahindra Bank, HDFC Bank, Federal Bank, Axis Bank and ICICI Bank gained 123 per cent, 104 per cent, 83 per cent, 37 per cent and 10 per cent, respectively.

In the PSU bank space, barring a few players such as Indian Bank (up 81 per cent), Vijaya Bank (up 46 per cent), Central Bank (up 32 per cent) and State Bank of India (up 7 per cent), other stocks slipped up to 68 per cent in this period. UCO Bank, Indian Overseas Bank, United Bank, Dena Bank and J&K Bank have been among the top losers.

Data available with RBI shows there were 1,35,946 bank branches in India as of March 2017 and 388 million and 28.30 million savings and current bank accounts, respectively. Public sector players hold the lion’s share of these bank accounts, especially after the Pradhan Mantri Jan Dhan Yojna (PMJDY) helped them notch up strong volumes within a short span of time.

More than three-fourths of the 69 lakh new accounts opened under the PMJDY between November 9 and December 28 went to the PSU banks, which added 54.52 lakh of these accounts. Nearly 37 lakh of them were from the urban areas.

Sectoral analysts say private lenders wanting to increase their penetration can find themselves with a big advantage on a platter as they can siege upon the bank account portability scheme with lucrative benefit to enter newer markets and enhance deposit base.

The PSU lenders also lag in terms of technology, which has already make banking transactions faster and easier and hugely enhanced the entire experience. This can be a big for customers to shift to private players if the PSU lenders fail to upgrade themselves quickly.

PSU lenders have also been facing other major issues in terms of mounting non-performing assets. Credit growth of PSU banks has declined to a multi-year low of 5.1 per cent on a year-on-year basis in FY17.

“Private sector banks will benefit the most from bank account number portability, as their services are far superior compared with that of PSU banks. However, the buzz will not make much difference in the market immediately,” said Ambareesh Baliga, an independent market analyst.

AK Prabhakar, Head of Research, IDBI Capital said, “Portability will give the power to customers to bargain for better facilities. The move will definitely benefit efficient banks.”

He advised investors to keep an eye on banks with robust balance sheets.

For the latest quarter ended March 31, 2017, gross non-performing assets of public sector banks climbed 4.77 per cent on a quarter-on-quarter basis to Rs 6.25 lakh crore from Rs 4.76 lakh crore as of December 2016.

Total GNPA of private sector banks stood at Rs 86,326 crore as of March 31, 2017 against Rs 81,252 crore in the sequential quarter ended December 2016.

In the last few years, PSU banks (with the exception of SBI) have steadily lost market shares to the private players, which have manage to make strong inroads with better services, higher capital and aggressive technology integration.

“PSU banks have lost around 430 basis points in systemic credit market share since FY15, mostly to new private sector banks,” brokerage ICICI Securities said in a recent research report.

The government has promised to infuse Rs 70,000 crore in the PSU lenders over 2016-2019, with Rs 10,000 crore allocated for each of financial year 2018 and 2019. “These amounts will not be sufficient to fully resolve the looming capital shortfall for the public sector banks,” rating agency S&P said.

“Private sector banks continue to be better positioned than their PSU peers on capital adequacy ratio (CAR), as better RoEs enable them to create capital. They are also effective in raising CET-I resources through regular dilution of equity at significantly book-accretive levels, largely to aid business growth momentum. PSU banks are witnessing higher capital burn on account of higher asset delinquencies. Furthermore, they remain dependant the Government of India for capital infusion amid adverse business conditions,” ICICI Securities said.

India allowed mobile phone subscribers to port their numbers last decade, while the Insurance Regulatory and Development Authority of India is considering a plan to allow life insurance policy holders to switch from one insurer to another without surrendering existing policies.

Industry experts say bank account portability will not be an easy task as Indian lenders use multiple account number formats. For instance, an ICICI Bank savings bank account has 12 digits, while Citibank issues 10-digit account numbers and HDFC Bank 14 digits.

“Practically, bank account number portability sounds difficult to implement,” said Ajay Jaiswal, Head of Research at Stewart & Mackertich.

A proposal for bank account number portability has come at the worst time for India’s public sector lenders, when they have been desperately looking for ways to get bad loans off their back and raise fresh capital to replenish coffers.

Reserve Bank of India (RBI) Deputy Governor SS Mundra dropped the bombshell on May 30, when he hinted that bank account number portability would be a reality soon.

Industry watchers say the move could prove back-breaking for the PSU lenders and is likely to put private sector lenders with a clear advantage, as they enjoy better operational freedom and are ahead technologically. Such a move can decisively take the banking turf away from the PSU lenders.

Banking analysts, however, say the proposal looks fine only on paper but will be tough to implement on the ground.

Since the arrival of the Narendra Modi-led NDA government on May 26, 2014, private sector banks have been continuously outperforming their public sector peers in the stock market by huge margins. Shares of IndusInd Bank, DCB Bank, Lakshmi Vilas Bank and YES Bank have surged over 150 per cent in the first three years of the Modi government.

ADVERTISEMENT

Other private sector bank majors such as Kotak Mahindra Bank, HDFC Bank, Federal Bank, Axis Bank and ICICI Bank gained 123 per cent, 104 per cent, 83 per cent, 37 per cent and 10 per cent, respectively.

In the PSU bank space, barring a few players such as Indian Bank (up 81 per cent), Vijaya Bank (up 46 per cent), Central Bank (up 32 per cent) and State Bank of India (up 7 per cent), other stocks slipped up to 68 per cent in this period. UCO Bank, Indian Overseas Bank, United Bank, Dena Bank and J&K Bank have been among the top losers.

Data available with RBI shows there were 1,35,946 bank branches in India as of March 2017 and 388 million and 28.30 million savings and current bank accounts, respectively. Public sector players hold the lion’s share of these bank accounts, especially after the Pradhan Mantri Jan Dhan Yojna (PMJDY) helped them notch up strong volumes within a short span of time.

More than three-fourths of the 69 lakh new accounts opened under the PMJDY between November 9 and December 28 went to the PSU banks, which added 54.52 lakh of these accounts. Nearly 37 lakh of them were from the urban areas.

ADVERTISEMENT

Sectoral analysts say private lenders wanting to increase their penetration can find themselves with a big advantage on a platter as they can siege upon the bank account portability scheme with lucrative benefit to enter newer markets and enhance deposit base.

The PSU lenders also lag in terms of technology, which has already make banking transactions faster and easier and hugely enhanced the entire experience. This can be a big for customers to shift to private players if the PSU lenders fail to upgrade themselves quickly.

ADVERTISEMENT

PSU lenders have also been facing other major issues in terms of mounting non-performing assets. Credit growth of PSU banks has declined to a multi-year low of 5.1 per cent on a year-on-year basis in FY17.

“Private sector banks will benefit the most from bank account number portability, as their services are far superior compared with that of PSU banks. However, the buzz will not make much difference in the market immediately,” said Ambareesh Baliga, an independent market analyst.

AK Prabhakar, Head of Research, IDBI Capital said, “Portability will give the power to customers to bargain for better facilities. The move will definitely benefit efficient banks.”

He advised investors to keep an eye on banks with robust balance sheets.

For the latest quarter ended March 31, 2017, gross non-performing assets of public sector banks climbed 4.77 per cent on a quarter-on-quarter basis to Rs 6.25 lakh crore from Rs 4.76 lakh crore as of December 2016.

Total GNPA of private sector banks stood at Rs 86,326 crore as of March 31, 2017 against Rs 81,252 crore in the sequential quarter ended December 2016.

In the last few years, PSU banks (with the exception of SBI) have steadily lost market shares to the private players, which have manage to make strong inroads with better services, higher capital and aggressive technology integration.

“PSU banks have lost around 430 basis points in systemic credit market share since FY15, mostly to new private sector banks,” brokerage ICICI Securities said in a recent research report.

The government has promised to infuse Rs 70,000 crore in the PSU lenders over 2016-2019, with Rs 10,000 crore allocated for each of financial year 2018 and 2019. “These amounts will not be sufficient to fully resolve the looming capital shortfall for the public sector banks,” rating agency S&P said.

“Private sector banks continue to be better positioned than their PSU peers on capital adequacy ratio (CAR), as better RoEs enable them to create capital. They are also effective in raising CET-I resources through regular dilution of equity at significantly book-accretive levels, largely to aid business growth momentum. PSU banks are witnessing higher capital burn on account of higher asset delinquencies. Furthermore, they remain dependant the Government of India for capital infusion amid adverse business conditions,” ICICI Securities said.

India allowed mobile phone subscribers to port their numbers last decade, while the Insurance Regulatory and Development Authority of India is considering a plan to allow life insurance policy holders to switch from one insurer to another without surrendering existing policies.

Industry experts say bank account portability will not be an easy task as Indian lenders use multiple account number formats. For instance, an ICICI Bank savings bank account has 12 digits, while Citibank issues 10-digit account numbers and HDFC Bank 14 digits.

“Practically, bank account number portability sounds difficult to implement,” said Ajay Jaiswal, Head of Research at Stewart & Mackertich.

Too busy to trade in stocks? Invest in Mutual Funds with ET Money!

Bookmark or read stories offline -

Download ET Markets APP

Download ET Markets APP

Related Articles

South Indian Bank raises FCNR deposit rate to 6.5 pc after RBI swap window2026-06-19T12:38:43Z

South Indian Bank raises FCNR deposit rate to 6.5 pc after RBI swap window2026-06-19T12:38:43Z- Sunil Singhania-backed Abakkus Flexi Cap Fund increases stake in HDFC Bank, RIL and 29 others in May2026-06-19T10:14:57Z

- Bandhan Bank increases FCNR(B) deposit rates to 7.1 pc after RBI forex swap move2026-06-19T09:10:08Z

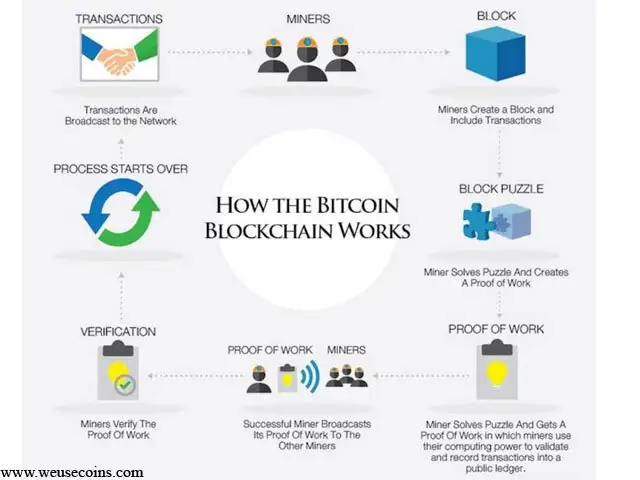

Bitcoin, the first decentralized digital currency, recently made news when it became the choice of currency for the cyber attackers who crippled computer networks around the world. After which, the value of the currency shot up and now stands at Rs 1,56,452.46 to even exceed the price of gold!

Here’s a look at the digital currency and what it means to investors

ADVERTISEMENT