Claiming deductions of more than Rs 2.5 lakh? You won’t gain from moving to the new tax regime

Highlights

- This threshold of Rs 2.5 lakh includes the standard deduction of Rs 50,000 for which no investment is required.

- If you are claiming more than Rs 50,000 as HRA exemption, or housing loan interest, or even the NPS contribution under Sec 80CCD(1b), you are better off in the existing structure.

This threshold of Rs 2.5 lakh includes the standard deduction of Rs 50,000 for which no investment is required. All salaried taxpayers are eligible for this, which leaves only an additional deduction of Rs 2 lakh. Of this, Rs 1.5 lakh is taken care of by the Sec 80C investments.

So if you are claiming more than Rs 50,000 as HRA exemption or housing loan interest, or even the NPS contribution under Sec 80CCD(1b), you are better off in the existing structure. All said and done, the new regime won’t help you much if you are a good investor and avid tax planner.

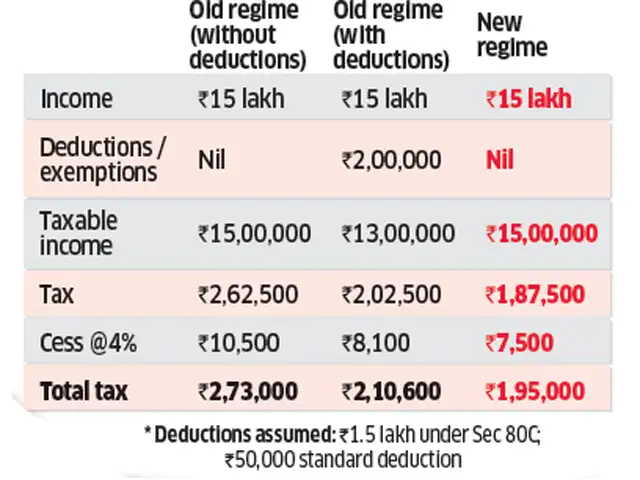

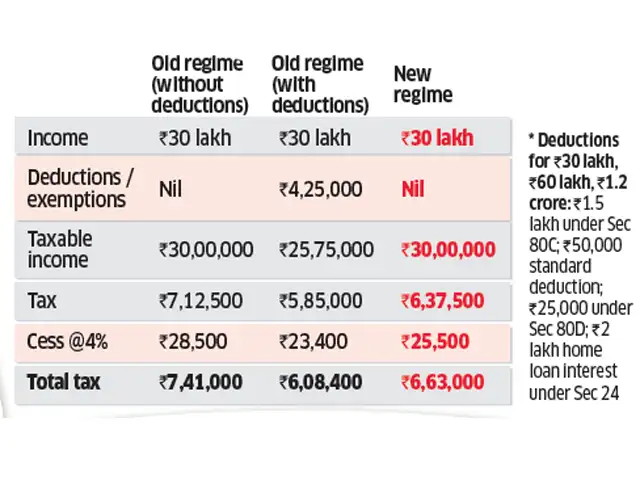

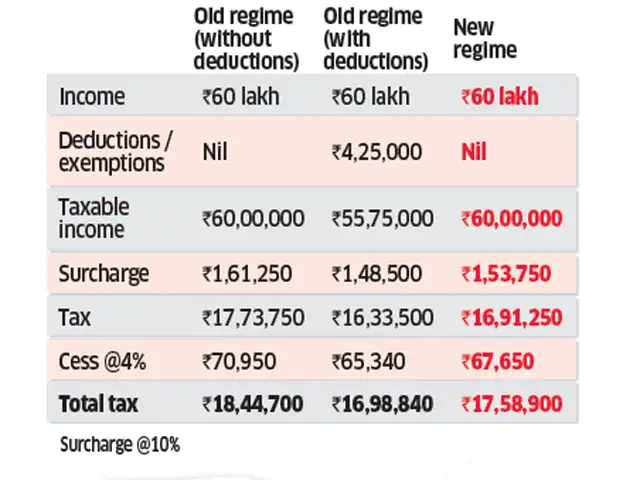

This threshold of Rs 2.5 lakh deduction applies to income above Rs 15 lakh. The breakeven point is even lower for those in the lower income brackets.

DON’T MOVE TO THE NEW REGIME IF YOU CLAIM MORE THAN THIS

| Gross annual income | Deductions claimed* | Existing tax | New tax |

| Rs 8 lakh | Rs 1.38 lakh | 46,800 | 46,800 |

| Rs 10 lakh | Rs 1.88 lakh | 78,000 | 78,000 |

| Rs 12 lakh | Rs 1.91 lakh | 1,19,600 | 1,19,600 |

| Rs 15 lakh | Rs 2.5 lakh | 1,95,000 | 1,95,000 |

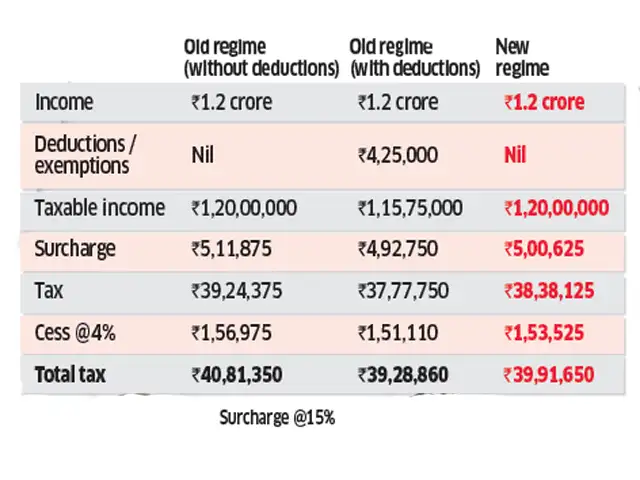

If the taxpayer is claiming more than the deductions mentioned in the table above, he stands to lose under the new regime. Finance Minister Nirmala Sitharaman said in her speech that a taxpayer earning Rs 15 lakh will save Rs 78,000 in tax under the new regime.

But this assumes the taxpayer is not claiming any deduction at all. In reality, the standard deduction applies automatically to all salaried taxpayers. Also, there are several expenses that are eligible for tax benefits, such as tuition fee of up to two children which can be claimed as a deduction under Sec 80C. There is also life and health insurance premiums and education loan interest, besides house rent and home loan interest.

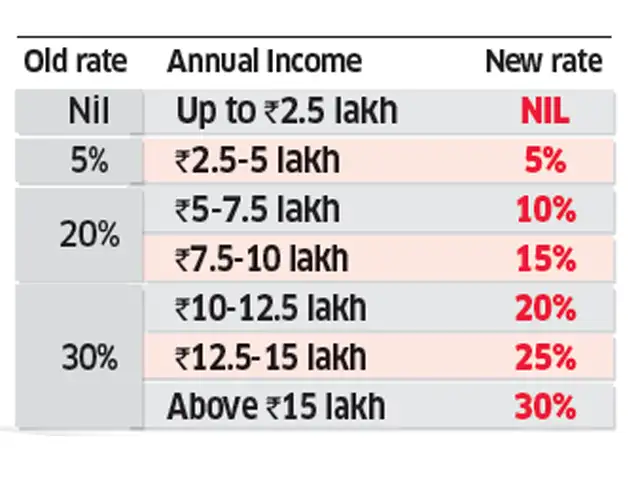

In Union Budget 2020, Nirmala Sitharaman introduced a "simplified", optional regime with three new tax slabs. However, taxpayers can continue with the existing structure if that suits them more. Although the doing away of exemptions and deductions simplifies compliance, taxpayers who exploited deductions to the fullest may pay more tax under the new regime. The budget has tried to put more money in the hands of taxpayers by curtailing the incentives to save.

The tax exemption given to incomes up to Rs 5 lakh remains unchanged. Salaried taxpayers who opt for the new regime will have to forgo standard deduction as well as exemptions under chapter VI-A, including HRA, investments under Section 80C, medical insurance premium and even leave travel allowance which is tax free, if claimed once in a block of two years.

The Economic Times Business News App for the Latest News in Business, Sensex, Stock Market Updates & More.

The Economic Times News App for Quarterly Results, Latest News in ITR, Business, Share Market, Live Sensex News & More.

Related Articles

Did you donate to a political party or plan to do so in the future and claim an income tax deduction? New ITR forms require extra disclosure, check what to report2026-04-08T06:03:58Z

Did you donate to a political party or plan to do so in the future and claim an income tax deduction? New ITR forms require extra disclosure, check what to report2026-04-08T06:03:58Z- Confused about income tax deduction on pre-EMI interest? Budget 2026 brings clarity on Rs 2 lakh home loan deduction2026-02-06T10:50:38Z

- Shinde wins Rs 1.4 lakh tax penalty case despite claiming false income tax deductions to reduce income by 50%; Know the details2025-07-24T03:41:00Z