What to do if you are mis-sold a financial product

Banks continue to mis-sell financial products basis their own commissions rather than the customer's needs. One can take these steps in case of such an event.

By Narendra Nathan, ET Bureau | Updated:

ThinkStock Photos

A bank branch is armed with relationship managers waiting to ‘sell’ unsuspecting customers financial products they may or may not need. Many, buy these products without knowing whether these fit their investment portfolios or risk profiles and end up with dud investments.

Here is a look at what you should do if you are mis-sold a product.

Insurance policies

Since mis-selling is rampant here, the regulator has kept a free look period of 15 days and some companies offer up to 30 days. Please note, this free look period is not from your date of application, but from the date you receive the policy document. If you have been mis-sold a policy, say a Ulip or an endowment plan, you can return it within the prescribed free look period.

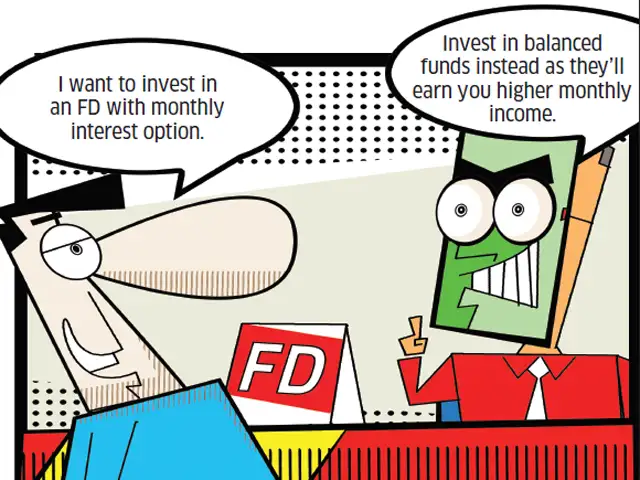

Balanced funds

If you have mis-sold balanced funds, immediate redemption will be a problem because most funds charge 1% exit load, if redeemed before one year. However, if your equity exposure has gone up significantly due to the balanced fund, you have no option but to redeem it and bear this exit load hit.

Fixed deposits at banks/NBFCs

If you are mis-sold an FD, premature withdrawal is the best solution. Since most banks charge just a small penalty on interest—the interest you get will be lower than contracted for—the chance of capital loss is less. You will be stuck if the mis-sold products are deposits from NBFCs because most NBFCs don’t offer premature withdrawals. And the ones that offer it, allow so only at quarterly intervals and also charge FD closure penalties of 1-3%.

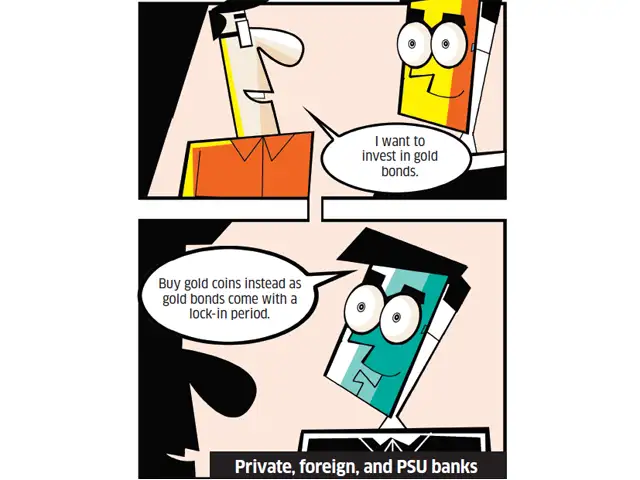

Gold bars/coins

In this case, immediate selling won’t be a good solution because the impact will be huge. Jewellers offer 5-10% less than the market price if you sell gold bars /coins to them and insist on money and not accept their offer of exchange for ornaments.

Here is a look at what you should do if you are mis-sold a product.

Insurance policies

Since mis-selling is rampant here, the regulator has kept a free look period of 15 days and some companies offer up to 30 days. Please note, this free look period is not from your date of application, but from the date you receive the policy document. If you have been mis-sold a policy, say a Ulip or an endowment plan, you can return it within the prescribed free look period.

Balanced funds

If you have mis-sold balanced funds, immediate redemption will be a problem because most funds charge 1% exit load, if redeemed before one year. However, if your equity exposure has gone up significantly due to the balanced fund, you have no option but to redeem it and bear this exit load hit.

Based on text by Narendra Nathan

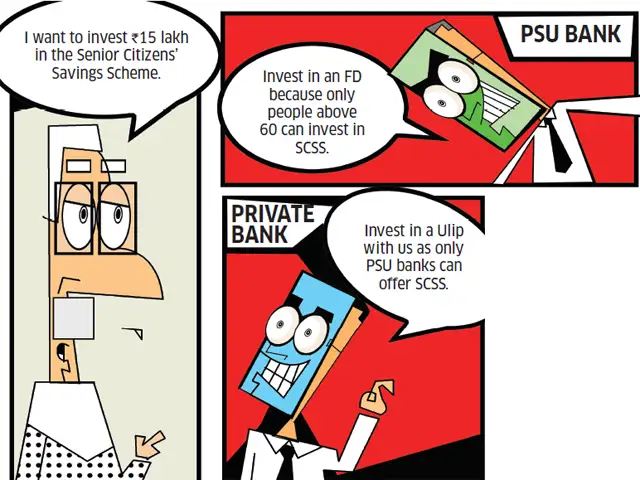

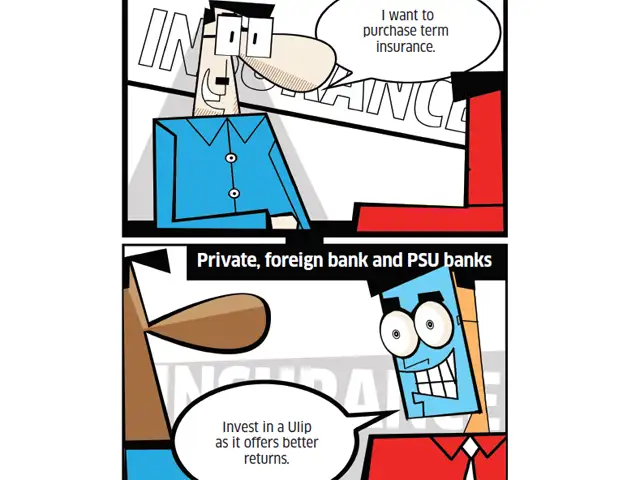

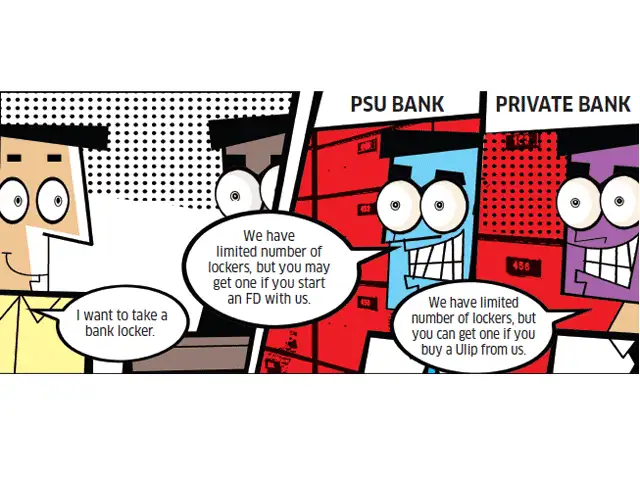

Bank officials still try to mislead people into buying products they don’t need. Banks also set stiff sales targets for relationship managers (RMs), forcing them to push products that fetch higher commissions, instead of investments that suit the investor’s needs. ET Wealth went undercover and found that bank executives continue to mis-sell insurance and other financial products.

Here is a look at how various financial products are mis-sold by bank executives.

Fixed deposits at banks/NBFCs

If you are mis-sold an FD, premature withdrawal is the best solution. Since most banks charge just a small penalty on interest—the interest you get will be lower than contracted for—the chance of capital loss is less. You will be stuck if the mis-sold products are deposits from NBFCs because most NBFCs don’t offer premature withdrawals. And the ones that offer it, allow so only at quarterly intervals and also charge FD closure penalties of 1-3%.

Gold bars/coins

In this case, immediate selling won’t be a good solution because the impact will be huge. Jewellers offer 5-10% less than the market price if you sell gold bars /coins to them and insist on money and not accept their offer of exchange for ornaments.

Download

The Economic Times Business News App for the Latest News in Business, Sensex, Stock Market Updates & More.

The Economic Times Business News App for the Latest News in Business, Sensex, Stock Market Updates & More.

Download

The Economic Times News App for Quarterly Results, Latest News in ITR, Business, Share Market, Live Sensex News & More.

The Economic Times News App for Quarterly Results, Latest News in ITR, Business, Share Market, Live Sensex News & More.

ADVERTISEMENT