Turning the black money tide: It will require reforms in taxation and real estate transactions

Generated through out-of-book transactions, under-reporting and market manipulation, black money distorts India’s financial regime.

By Varun Gandhi, TNN | Updated:

Voltaire wrote “If you see a Swiss banker jumping out of a window, follow him, there is sure to be a profit in it”. Following this train of thought India is seen to be ruined by a cartel of Swiss bankers, terrorists and corrupt industrialists. Unlimited black money is apparently out there, the “hidden hand” behind all unfortunate events to befall our Republic.

A new government need only knock at Swiss banks for untold wealth to be ecured. So goes modern India’s debate on black money. The “hidden hand”, however, needs more definition.

Generated through out-of-book transactions, under-reporting, hawala, international transactions and market manipulation, black money distorts India’s financial regime. While proposed cash restrictions (which could be capped at Rs 10 lakh) and PAN card authentication should limit such transfers, allowing enforcement agencies to act against violators and seize unaccounted currency, offshore banking will still prevail. Without significant penalties (under discussion), black money will flow.

Swiss rumours abound, stating amounts upwards of $20 tn. The Swiss National Bank stated that the total liabilities of Swiss Banks towards Indians were $2.5 bn, just 0.07% of total bank deposits. Under the Double Taxation Agreement with Switzerland, information is shared only if offences are proven and are of criminal nature, making information gathering a tedious affair. Confidentiality issues and disclosures clauses in signed international treaties make revealing any names a tricky affair for the government.

According to the Department of Industrial Policy and Promotion, Mauritius and Singapore, with their small economies, account for the majority of FDI received by India. FII investments held through P-Notes stood at Rs 2.65 lakh crore, an 80-month high in October 2014.

While FIIs are required to report investor identities on a monthly basis, it is possible to hide beneficiary identities through multiple layers. Global depository receipts issued by some Indian companies, listed on the Luxembourg Stock Exchange, can be used to manipulate markets.

Charitable organisations receiving foreign contributions are required to provide an annual return to the ministry of home affairs, without any mention of benefitted recipients. For the determined entity, multiple avenues exist.

Policy incentives matter. India’s black money strategy should consider four pillars. It could encourage tax rate rationalisation, reform vulnerable sectors, support a cashless economy and create effective and credible deterrence.

Tax rate rationalisation, with lower tax rates as an end goal, would increase the tax base and increase compliance with tax returns. Transaction costs can be curbed by a simplification of the taxation regime and its myriad mazes. The introduction of GST will significantly discourage out-of-book sales.

The inefficient real estate sector constitutes nearly 11% of India’s GDP. Given high stamp duties which are set by state governments, underreporting of transactions is quite common. Restricting stamp duty taxes to 5% along with repealing the Urban Land Ceiling Regulation Act and reform of the Rent Control Act can reduce this. Expanding the Property Title Certification system in urban local bodies and computerisation of land registration and property would regulate financing.

A new government need only knock at Swiss banks for untold wealth to be ecured. So goes modern India’s debate on black money. The “hidden hand”, however, needs more definition.

Generated through out-of-book transactions, under-reporting, hawala, international transactions and market manipulation, black money distorts India’s financial regime. While proposed cash restrictions (which could be capped at Rs 10 lakh) and PAN card authentication should limit such transfers, allowing enforcement agencies to act against violators and seize unaccounted currency, offshore banking will still prevail. Without significant penalties (under discussion), black money will flow.

Swiss rumours abound, stating amounts upwards of $20 tn. The Swiss National Bank stated that the total liabilities of Swiss Banks towards Indians were $2.5 bn, just 0.07% of total bank deposits. Under the Double Taxation Agreement with Switzerland, information is shared only if offences are proven and are of criminal nature, making information gathering a tedious affair. Confidentiality issues and disclosures clauses in signed international treaties make revealing any names a tricky affair for the government.

According to the Department of Industrial Policy and Promotion, Mauritius and Singapore, with their small economies, account for the majority of FDI received by India. FII investments held through P-Notes stood at Rs 2.65 lakh crore, an 80-month high in October 2014.

While FIIs are required to report investor identities on a monthly basis, it is possible to hide beneficiary identities through multiple layers. Global depository receipts issued by some Indian companies, listed on the Luxembourg Stock Exchange, can be used to manipulate markets.

ADVERTISEMENT

Charitable organisations receiving foreign contributions are required to provide an annual return to the ministry of home affairs, without any mention of benefitted recipients. For the determined entity, multiple avenues exist.

Policy incentives matter. India’s black money strategy should consider four pillars. It could encourage tax rate rationalisation, reform vulnerable sectors, support a cashless economy and create effective and credible deterrence.

Tax rate rationalisation, with lower tax rates as an end goal, would increase the tax base and increase compliance with tax returns. Transaction costs can be curbed by a simplification of the taxation regime and its myriad mazes. The introduction of GST will significantly discourage out-of-book sales.

The inefficient real estate sector constitutes nearly 11% of India’s GDP. Given high stamp duties which are set by state governments, underreporting of transactions is quite common. Restricting stamp duty taxes to 5% along with repealing the Urban Land Ceiling Regulation Act and reform of the Rent Control Act can reduce this. Expanding the Property Title Certification system in urban local bodies and computerisation of land registration and property would regulate financing.

ADVERTISEMENT

Transitioning beyond the cash economy is necessary, through reduction of high-end denominations (Rs 1000 and Rs 500) along with, as is being considered, legally restricting keeping very large amounts of cash with oneself. The government should consider amending existing laws, including the Coinage Act (2011), the Reserve Bank of India Act (1934) and FEMA, while enacting an entirely new statute aimed at regulating the possession and transportation of cash above a particular threshold limit.

Implementation of the Electronic Delivery of Services Bill (2011) that requires the delivery of various public services through digital means will go a long way. Banking channels including credit and debit cards may be promoted through tax incentives, along with Indian e-service intermediaries like Ru-Pay. The government has done well to introduce the Jan Dhan Yojana bringing 10.3 crore individuals under the formal banking system.

Without deterrence, most reform is for nought. Much can be done by simply improving our taxation systems. The direct tax administration’s Directorate of Criminal Investigation needs to be provided the right IT training, infrastructure and funding to become an effective deterrent. The Large Taxpayer Units can become more effective in investigating corporates if audit cycles of income tax, service tax and excise tax departments are aligned, increasing the scope of simultaneous scrutiny and examination.

There is no magic wand. Broken institutions require bolstering, while international finance requires patience to navigate. Pursuing significant evaders requires social cooperation and a change in our political culture. Social mores against corporate bankruptcy need to be overturned. Honesty can stare dishonesty out of countenance.

Download

The Economic Times Business News App for the Latest News in Business, Sensex, Stock Market Updates & More.

The Economic Times Business News App for the Latest News in Business, Sensex, Stock Market Updates & More.

Download

The Economic Times News App for Quarterly Results, Latest News in ITR, Business, Share Market, Live Sensex News & More.

The Economic Times News App for Quarterly Results, Latest News in ITR, Business, Share Market, Live Sensex News & More.

Related Articles

Updated return vs black money law: Drafting gap may trigger 30% tax and 300% penalty under Finance Bill 20262026-03-06T01:31:00Z

Updated return vs black money law: Drafting gap may trigger 30% tax and 300% penalty under Finance Bill 20262026-03-06T01:31:00Z- ₹60 Lakh vs ₹1.20 crore: How Budget 2026’s foreign asset disclosure scheme cuts black money act risk for NRIs and residents with overseas assets2026-03-04T07:01:22Z

- Delhi High Court stays Black Money Act action on ‘involuntary residents’ in Rajiv Saxena Case2026-02-27T00:30:00Z

ET Bureau

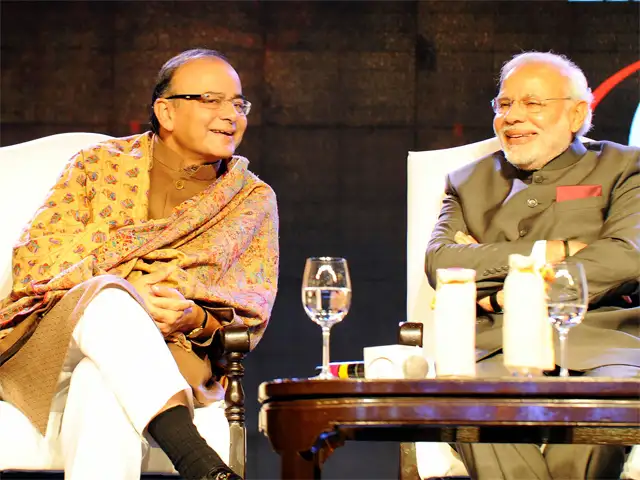

The Economic Times Global Business Summit turned out to be one of its kind of forum – full of unexpected delights and charms. From PM Narendra Modi setting a $20-trillion target for the economy, to his ministers painting a picture of how they will work to realise the dream, we take a look at the biggest takeaways from a forum that had the best of thought leaders and corporate minds debating on how to script an economic change...

In pic: Times Group MD Vineet Jain welcomes Prime Minister Narendra Modi, the man of the moment, with a shawl at the ET Global Economic Summit.

Don't miss the full coverage of the Summit

The Economic Times Global Business Summit turned out to be one of its kind of forum – full of unexpected delights and charms. From PM Narendra Modi setting a $20-trillion target for the economy, to his ministers painting a picture of how they will work to realise the dream, we take a look at the biggest takeaways from a forum that had the best of thought leaders and corporate minds debating on how to script an economic change...

In pic: Times Group MD Vineet Jain welcomes Prime Minister Narendra Modi, the man of the moment, with a shawl at the ET Global Economic Summit.

Don't miss the full coverage of the Summit

ADVERTISEMENT