IPO watch: Healthy business, reasonable pricing make CDSL a good bet

Through OFS, the BSE is set to reduce its stake in CDSL from the current 50% to 24%.

By Devangi Gandhi, ET Bureau | Updated:

ET Intelligence Group: The primary market debut of Central Depository Services Ltd ( CDSL) is a good opportunity for investors looking to benefit from the increasing penetration of financial investments in India. Healthy fundamentals and reasonable pricing make it an attractive bet even as revenue growth will continue to depend on popularity of the capital markets, especially equities.

Through offer for sale (OFS), the Bombay Stock Exchange is set to reduce its stake in CDSL from the current 50% to 24%. State Bank of India, Bank of Baroda and Calcutta Stock Exchange will also participate in the issue. Of the total issue size (3.52 crore shares), 34% is available for retail investors.

At the upper band of the offer price of Rs 149, the issue is priced at 18 times FY17 earnings which is not expensive, although it is at a steep 89% premium to the last transaction in which BSE offered 4.15% stake in the company to LIC in October last year at Rs 79 per share.

BUSINESS

CDSL is one of the two depository services operating in India. It provides dematerialisation of a wide range of products including securitises, mutual fund units and debt instruments. It provides KYC services, supports transaction related to corporate actions like bonus and mergers and helps insurance companies in holding policies in electronic formats. Its revenue from operations consists of transaction charges, account maintenance and settlement charges, corporate action charges and e-voting charges. It has 44% market share in terms of total demat accounts in FY17, compared to 40% in FY13. In the past four years, CDSL has gained higher proportion of incremental demat accounts.

FINANCE

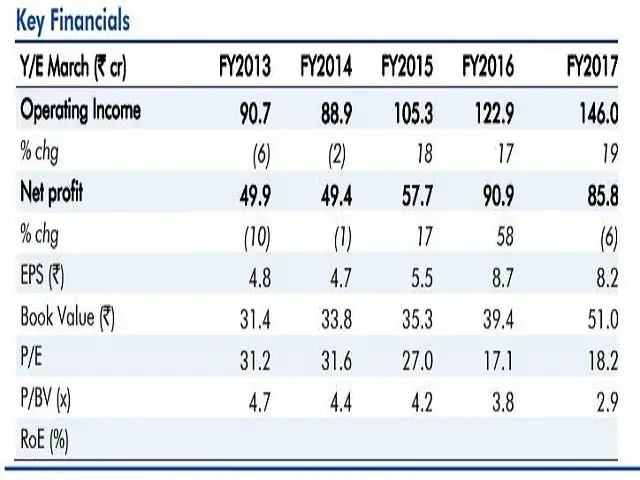

CDSL's operating income has grown at annual rate of 17% in the last two financial years to Rs 146 crore. The operating profit before exceptional items and net profit have grown by 21% and 23%, respectively, during the period. In FY17, reported net profit was Rs 86.6 crore, 5% lower than in FY16 when it reported exceptional gains of Rs 33 crore, due to the reversal of required transfer to Investor Education and Protection Fund which was reduced from 25% of total income to 5% of operating income. The company boasts operating margin of 80% and net profit margin of 46% in FY17.

RECOMMENDATIONS

Angel Broking Recommendation: Subscribe

The retail brokerage said CDSL has a unique business model with high-entry barriers, limited capital required for doing business and a wide base of revenue sources.The brokerage expects growth to sustain due to buoyant markets and increasing share of savings moving into the financial space.The average return on equity of around 17% in the last six years will sustain going ahead as well, it said, adding that the valuation is reasonable.

Equinomics Research and Advisory Recommendation: Subscribe

CDSL's generous dividend policy makes the stock a long-term portfolio bet, said Equinomics Research. CDSL's dividend payout was 39% of earnings in financial year 2014-15 and 29% in financial year 2015-16. Investors into equities are growing steadily in India, which is a positive development for the long-term growth of the depository .

IIFL Recommendation: Subscribe

Citing strong fundamentals and clean balance sheet, the brokerage recommends buying into the IPO.

Besides stable income sources, low operational costs support CDSL with ro bust margins, said IIFL. The brokerage said that CDSL is debt free and giving consist ent dividend payouts at 3550% of the net income over the last three years owing to steady growth in revenue.

LKP Securities Recommendation: Subscribe

The brokerage said CDSL is the perfect pick to play out the structural growth story of securities markets in India as increasing financial literacy and urbanisation are likely to augment demand for demat accounts. CDSL will continue to grab bigger market share of incremental demat accounts due to its lower networth and reserve requirements as well as wide geographic coverage, the brokerage said.

Motilal Oswal Recommendation: Subscribe

The domestic brokerage views CDSL as a long-term investment.The brokerage said CDSL has controlled operating expenses in the last three years, which is a key positive as it has led to margin expansion of 1,150 basis points since 2014-15 financial year to 54% in the financial year ended March.Strong parentage, entry barrier and margins along with stable earnings growth make the valuation attractive.

Through offer for sale (OFS), the Bombay Stock Exchange is set to reduce its stake in CDSL from the current 50% to 24%. State Bank of India, Bank of Baroda and Calcutta Stock Exchange will also participate in the issue. Of the total issue size (3.52 crore shares), 34% is available for retail investors.

At the upper band of the offer price of Rs 149, the issue is priced at 18 times FY17 earnings which is not expensive, although it is at a steep 89% premium to the last transaction in which BSE offered 4.15% stake in the company to LIC in October last year at Rs 79 per share.

BUSINESS

CDSL is one of the two depository services operating in India. It provides dematerialisation of a wide range of products including securitises, mutual fund units and debt instruments. It provides KYC services, supports transaction related to corporate actions like bonus and mergers and helps insurance companies in holding policies in electronic formats. Its revenue from operations consists of transaction charges, account maintenance and settlement charges, corporate action charges and e-voting charges. It has 44% market share in terms of total demat accounts in FY17, compared to 40% in FY13. In the past four years, CDSL has gained higher proportion of incremental demat accounts.

FINANCE

ADVERTISEMENT

CDSL's operating income has grown at annual rate of 17% in the last two financial years to Rs 146 crore. The operating profit before exceptional items and net profit have grown by 21% and 23%, respectively, during the period. In FY17, reported net profit was Rs 86.6 crore, 5% lower than in FY16 when it reported exceptional gains of Rs 33 crore, due to the reversal of required transfer to Investor Education and Protection Fund which was reduced from 25% of total income to 5% of operating income. The company boasts operating margin of 80% and net profit margin of 46% in FY17.

RECOMMENDATIONS

Angel Broking Recommendation: Subscribe

The retail brokerage said CDSL has a unique business model with high-entry barriers, limited capital required for doing business and a wide base of revenue sources.The brokerage expects growth to sustain due to buoyant markets and increasing share of savings moving into the financial space.The average return on equity of around 17% in the last six years will sustain going ahead as well, it said, adding that the valuation is reasonable.

Equinomics Research and Advisory Recommendation: Subscribe

ADVERTISEMENT

CDSL's generous dividend policy makes the stock a long-term portfolio bet, said Equinomics Research. CDSL's dividend payout was 39% of earnings in financial year 2014-15 and 29% in financial year 2015-16. Investors into equities are growing steadily in India, which is a positive development for the long-term growth of the depository .

IIFL Recommendation: Subscribe

ADVERTISEMENT

Citing strong fundamentals and clean balance sheet, the brokerage recommends buying into the IPO.

Besides stable income sources, low operational costs support CDSL with ro bust margins, said IIFL. The brokerage said that CDSL is debt free and giving consist ent dividend payouts at 3550% of the net income over the last three years owing to steady growth in revenue.

LKP Securities Recommendation: Subscribe

The brokerage said CDSL is the perfect pick to play out the structural growth story of securities markets in India as increasing financial literacy and urbanisation are likely to augment demand for demat accounts. CDSL will continue to grab bigger market share of incremental demat accounts due to its lower networth and reserve requirements as well as wide geographic coverage, the brokerage said.

Motilal Oswal Recommendation: Subscribe

The domestic brokerage views CDSL as a long-term investment.The brokerage said CDSL has controlled operating expenses in the last three years, which is a key positive as it has led to margin expansion of 1,150 basis points since 2014-15 financial year to 54% in the financial year ended March.Strong parentage, entry barrier and margins along with stable earnings growth make the valuation attractive.

Too busy to trade in stocks? Invest in Mutual Funds with ET Money!

Bookmark or read stories offline -

Download ET Markets APP

Download ET Markets APP

Related Articles

Jio Platforms plans $3 billion debt reduction from IPO proceeds2026-06-20T12:11:21Z

Jio Platforms plans $3 billion debt reduction from IPO proceeds2026-06-20T12:11:21Z- NSE's Rs 30,000 crore IPO set to spotlight exchange's dominance in Indian markets, dependence on options trading: Zerodha analysis2026-06-20T12:02:55Z

- Free shares! NSE IPO DRHP reveals curious case of 5,000 shares landing in wrong demat account2026-06-20T10:09:10Z

The stock is offered at 17.7-18.2x its FY2017 EPS and an issue price band of Rs 145-149.

Here's everything you should know if you are planning on investing.

ADVERTISEMENT