CreditAccess Grameen IPO kicks off; should you give it a miss?

At the upper price band of Rs 422, the issue is valued at 2.9 times post issue book value.

By Amit Mudgill, ETMarkets.com | Updated:

ThinkStock Photos

NEW DELHI: CreditAccess Grameen, a micro finance institution, came out with its initial public offering on Wednesday.

The MFI on Tuesday allotted 80,41,617 equity shares to 21 anchor investors at Rs 422 per scrip, garnering Rs 339.36 crore. The list included ICICI Prudential Banking and Financial Services Fund, Sundaram Mutual Fund, Citigroup Global Markets Mauritius and BNP Paribas Arbitrage.

Brokerages said that the company's strong customer connect in rural India, as suggested by retention ratio, a well-capitalised balance sheet and strong operations make a case for subscribe, but its high geographic concentration (84 per cent assets in Karnataka and Maharashtra) and inability to offer di versified products raise long-term growth concerns.

A few brokerages believe investors can give this IPO a miss while others say they still subscribe, but with caution.

At the upper limit of price band Rs 418-422 per share, the issue is valued at 2.9 times post issue book value, which is premium to peers Ujjivan Financial (at 2.7 times) and Equitas (2.8 times).

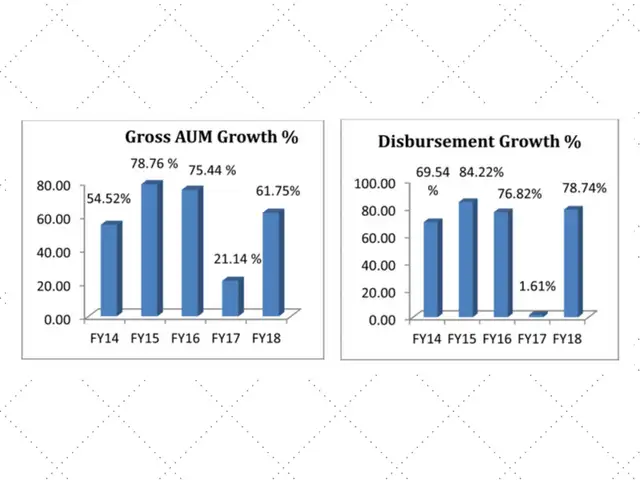

The company reported 65.2 per cent compounded annual growth rate in net assets under management (AUM) and 56 per cent growth in disbursements from FY14 to FY18. This is even as the actual count of customers for the same period has increased by 32.4 per cent, analysts noted.

"This particularly creates two probable scenarios for growth: Either the company has been disbursing incremental loans to same set of customers or the overall ticket size has seen a rapid rise. Both this probabilities indicates exposure to overleveraged customer base which possess higher risk of future defaults," said Emkay Global in a note.

The brokerage said that even as the management has actively denied any incremental MFI loan to same customer till original loan has been repaid, the probability of MFI offering additional loan under different segment is still there. This further accelerates overall concentration risk for the company, it said.

Antique Stock Broking said the near-term outlook looks great for the MFI, thanks to huge capital infusion and strong growth. "However, the long term needs hard thinking – demonetisation has illustrated that even well run MFIs can lose 5-10 per cent of AUMs in crisis. Geographic diversification and well-capitalised balance sheet are the two most important defenses for NBFC-MFIs, who have regional niches. This will increase opex and cap RoEs. Valuations at 2.3 times FY20 book and 16 times earnings do not leave investors with much margin of safety," the brokerage said. This brokerage has recommended avoid on the issue.

CreditAccess Grameen was the second-largest MFI based on the loan amount disbursement in FY17 and was third largest company based on gross loan portfolio (GLP) as of March 31.

There is a new kid on the IPO block. CreditAccess Grameen, which deals in microfinance, kicks off its public share sale on Wednesday. Brokerage Hem Securities has a 'Subscribe' on the issue, but with limited upside potential. There's a catch, right? Let's take the curtain off.

The company’s focus customer segment is women with an annual household income of Rs 1.6 lakh or less in urban areas and Rs 1 lakh or less in rural areas. The loans are offered to women, who are willing to borrow in a group and are agreeable to accept joint liability for the loans under Joint Liability Group (JLG) model. Besides, the company also offers individual retail finance loans on a pilot basis for existing customers with at least three years of healthy track record.

"Some of the MFI converted SFB have been trying to scale down their MFI portfolio, due to volatility in the asset quality as well to scale up in other areas. However, we feel MFI as a segment is here to stay in India.

At the upper end of the price band, the issue is offered at 3.8 times its pre-issue BV. While the FY18 ROE of 11.8 per cent is still suboptimal compared to some of the large MFIs, we feel the valuation adequately captures this and any improvement in the ROE will aid to further valuations," SMC Institutional equities said in a note.

On the post dilution basis, the issue is available at 2.9 times BV (at upper limit). Angel Broking has subscribe rating on the issue while Choice Broking has advised "subscribe with caution.

"At these valuations, the issue presents limited room for further upside. Considering all these parameters, we assign ‘Subscribe with Caution’ rating to the issue. However, we think that business’s fundamentals are strong and it will create value in the short to medium term. Investors are thus recommended to invest in this issue for short to medium term period," Choice Broking said.

The MFI on Tuesday allotted 80,41,617 equity shares to 21 anchor investors at Rs 422 per scrip, garnering Rs 339.36 crore. The list included ICICI Prudential Banking and Financial Services Fund, Sundaram Mutual Fund, Citigroup Global Markets Mauritius and BNP Paribas Arbitrage.

Brokerages said that the company's strong customer connect in rural India, as suggested by retention ratio, a well-capitalised balance sheet and strong operations make a case for subscribe, but its high geographic concentration (84 per cent assets in Karnataka and Maharashtra) and inability to offer di versified products raise long-term growth concerns.

A few brokerages believe investors can give this IPO a miss while others say they still subscribe, but with caution.

At the upper limit of price band Rs 418-422 per share, the issue is valued at 2.9 times post issue book value, which is premium to peers Ujjivan Financial (at 2.7 times) and Equitas (2.8 times).

The company reported 65.2 per cent compounded annual growth rate in net assets under management (AUM) and 56 per cent growth in disbursements from FY14 to FY18. This is even as the actual count of customers for the same period has increased by 32.4 per cent, analysts noted.

ADVERTISEMENT

"This particularly creates two probable scenarios for growth: Either the company has been disbursing incremental loans to same set of customers or the overall ticket size has seen a rapid rise. Both this probabilities indicates exposure to overleveraged customer base which possess higher risk of future defaults," said Emkay Global in a note.

The brokerage said that even as the management has actively denied any incremental MFI loan to same customer till original loan has been repaid, the probability of MFI offering additional loan under different segment is still there. This further accelerates overall concentration risk for the company, it said.

Antique Stock Broking said the near-term outlook looks great for the MFI, thanks to huge capital infusion and strong growth. "However, the long term needs hard thinking – demonetisation has illustrated that even well run MFIs can lose 5-10 per cent of AUMs in crisis. Geographic diversification and well-capitalised balance sheet are the two most important defenses for NBFC-MFIs, who have regional niches. This will increase opex and cap RoEs. Valuations at 2.3 times FY20 book and 16 times earnings do not leave investors with much margin of safety," the brokerage said. This brokerage has recommended avoid on the issue.

CreditAccess Grameen was the second-largest MFI based on the loan amount disbursement in FY17 and was third largest company based on gross loan portfolio (GLP) as of March 31.

ADVERTISEMENT

The company’s focus customer segment is women with an annual household income of Rs 1.6 lakh or less in urban areas and Rs 1 lakh or less in rural areas. The loans are offered to women, who are willing to borrow in a group and are agreeable to accept joint liability for the loans under Joint Liability Group (JLG) model. Besides, the company also offers individual retail finance loans on a pilot basis for existing customers with at least three years of healthy track record.

ADVERTISEMENT

A few brokerages still remained positive on the MFI prospects."Some of the MFI converted SFB have been trying to scale down their MFI portfolio, due to volatility in the asset quality as well to scale up in other areas. However, we feel MFI as a segment is here to stay in India.

At the upper end of the price band, the issue is offered at 3.8 times its pre-issue BV. While the FY18 ROE of 11.8 per cent is still suboptimal compared to some of the large MFIs, we feel the valuation adequately captures this and any improvement in the ROE will aid to further valuations," SMC Institutional equities said in a note.

On the post dilution basis, the issue is available at 2.9 times BV (at upper limit). Angel Broking has subscribe rating on the issue while Choice Broking has advised "subscribe with caution.

"At these valuations, the issue presents limited room for further upside. Considering all these parameters, we assign ‘Subscribe with Caution’ rating to the issue. However, we think that business’s fundamentals are strong and it will create value in the short to medium term. Investors are thus recommended to invest in this issue for short to medium term period," Choice Broking said.

Too busy to trade in stocks? Invest in Mutual Funds with ET Money!

Bookmark or read stories offline -

Download ET Markets APP

Download ET Markets APP

ADVERTISEMENT